Fintech: How Tokenised Carbon Credits Could Transform Green Finance[1]

By Kabo Phage and Mpumi Ngwenya | March 2026

KABO PHAGE

FinTech Analyst | SARB |

|

MPUMI NGWENYA

Financial Markets Specialist | SARB |

1. Introduction: Climate Risk Meets Fintech

Climate change is now a material source of financial risk. As physical and transition risks intensify, regulators and central banks are embedding climate considerations into supervision, stress testing, and disclosure requirements

[2],[3]. Global initiatives such as the Task Force on Climate‑related Financial Disclosures (TCFD), the EU Sustainable Finance Taxonomy and the International Sustainability Standards Board (ISSB) climate standards are reshaping sustainable finance, increasing demand for credible, transparent, and scalable green finance mechanisms[4],[5].

In this context, financial technology (fintech) - including the use of digital tools such as blockchain, artificial intelligence, and data analytics in financial services - has emerged as a key enabler of green finance[6]. A prominent use case is tokenising carbon credits: representing verified emissions reductions as digital tokens on distributed ledgers. In principle, tokenisation can streamline issuance, trading, tracking, and retirement, while strengthening transparency and traceability across carbon markets[7].

Tokenised credits could broaden participation by lowering transaction costs and enabling access for retail investors and small and medium‑sized enterprises (SMEs). But they also introduce risks: unequal access to digital infrastructure, the environmental footprint of certain technologies, data governance and cybersecurity concerns, and greenwashing if standards and oversight are weak[8]. Designing markets that protect environmental integrity and financial stability is therefore essential, particularly in emerging markets.

Using tokenised carbon credits as a case study, this blog considers how fintech can improve access, transparency and efficiency in green finance, and highlights regulatory and policy considerations relevant for South Africa.

2. South Africa's Climate Risk Profile

South Africa faces significant climate related risks, stemming from environmental fragility and a carbon intensive economy. Key physical risks include water scarcity and shifting rainfall patterns. Rising temperatures and increased rainfall variability have contributed to more frequent droughts and floods, threatening water availability and food security. Semi-arid agricultural regions are increasingly exposed to crop failures and land degradation, placing pressure on rural livelihoods. At the same time, transition risks are material. South Africa's heavy reliance on coal fired power generation means that decarbonising the energy sector must be carefully managed to preserve energy security and support a just transition for affected workers and communities.

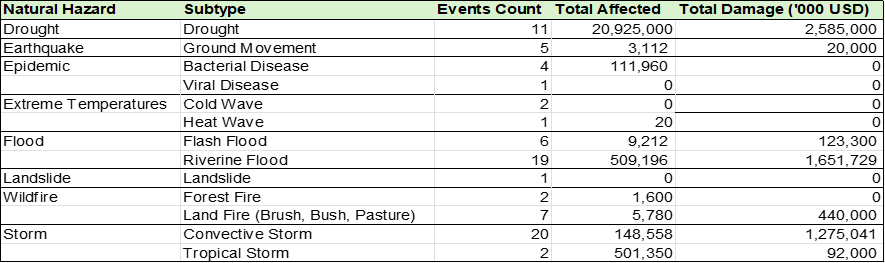

To contextualise these risks, data from the Emergency Events Database (EM-DAT) indicate that South Africa has experienced a wide range of natural hazards over the period 1900-2020 (see Table 1).

Table 1: Natural Disasters in South Africa

Source: Emergency Events Database

Table 1 highlights exposure to both acute shocks (storms and floods) and slow-onset risks (drought). Beyond humanitarian impacts, repeated events can increase fiscal pressures, disrupt agriculture and infrastructure, and transmit into financial stability through higher insurance losses, changing credit risk and shifting investment patterns.

2.1 From Climate Risks to Green Finance

These physical and transition climate risks highlight the need for financing mechanisms that can mobilise capital at scale while improving resilience and accountability, positioning tokenised carbon markets as a relevant sustainable finance use case in South Africa. By digitising verified emissions reductions, tokenised carbon credits can broaden investor participation - including institutions, SMEs and retail investors - and expand private capital for mitigation and adaptation projects. In the face of growing fiscal and macro‑financial pressures from floods, droughts and storms, more efficient and liquid carbon markets can help channel funding toward emissions reduction and climate resilient activities such as access to green financial products (Springer, 2025)[9]

2.1.1

Tokenised Carbon Markets as a Catalyst for Inclusive Green Finance

Retail investors and SMEs are often excluded from green finance because of high entry barriers and complex investment processes, including large minimum investment thresholds and limited secondary market liquidity[10]. Fintech innovation - particularly in the form of tokenised carbon markets - offers a pathway to overcome these constraints. Digital platforms and mobile applications reduce transaction costs and simplify participation, while blockchain infrastructure enables the tokenisation of carbon credits into smaller, tradeable units. This allows retail investors and SMEs to gain fractional exposure to green finance assets and to participate in peer‑to‑peer trading with greater liquidity and transparency. In parallel, alternative data and AI‑driven analytics can be embedded into these platforms to assess project impact, verify emissions outcomes and evaluate counterparty risk. Together, these fintech enabled market innovations expand access, lower barriers to entry and support a more inclusive and efficient green finance ecosystem (World Bank & IFC, 2022)[11].

3. Responding to South Africa's Climate Risks through Green Finance

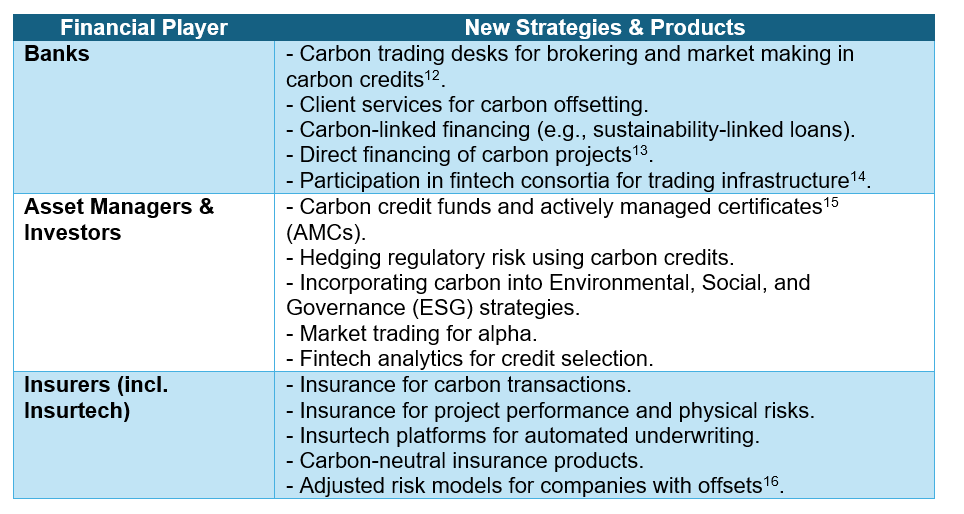

South Africa's financial institutions are responding to carbon market opportunities by combining fintech tools with traditional finance. Banks are exploring blockchain-based settlement and carbon trading services; asset managers use data tools (including satellite imagery) to support credit verification; and insurers apply climate analytics to price risk (Table 2). Together, these approaches aim to strengthen market confidence and expand green finance products.

Table 2: Financial sector players and their carbon market strategies[12],[13],[14],[15][16]

Source[17]: Standard Bank Group (2024–2025); Sofala Partners (2025); Orpheus Capital (2024); Howden Group (2024)

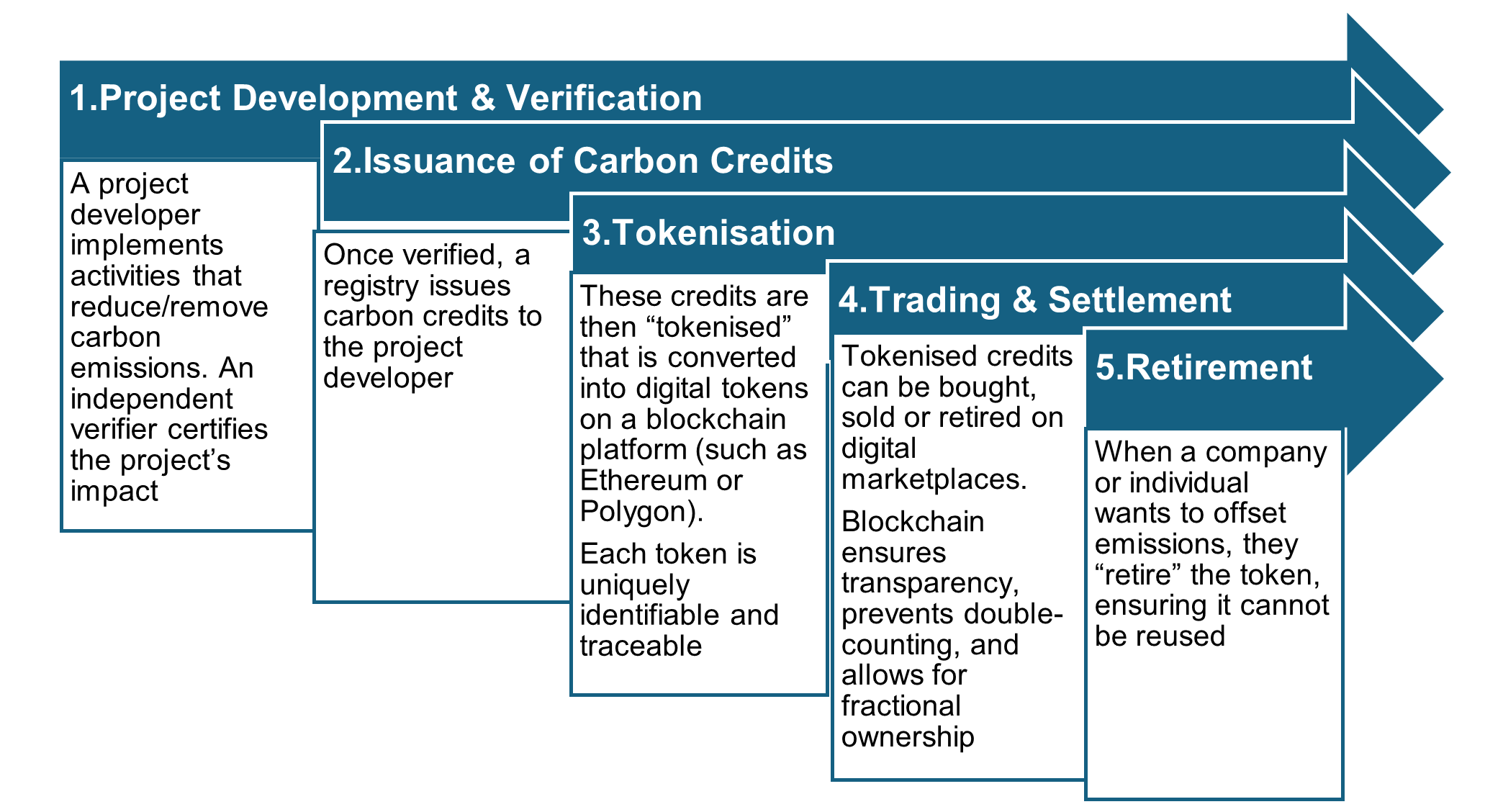

4. Tokenised Carbon Credits: Process and Benefits

Tokenisation converts a real-world asset, such as a carbon credit into a digital token recorded on a blockchain. Each token typically represents one verified ton of carbon dioxide CO₂ reduced or removed from the atmosphere. While it does not remove the upstream costs of developing and certifying projects, tokenisation can improve downstream market infrastructure by reducing trading, settlement and intermediation frictions. Figure 1 summarises a typical tokenisation flow.

Figure 1: The tokenisation process

Source: World Bank (2024)[18]

4.1 Benefits of Carbon Credit Tokenisation

Increased Accessibility and Liquidity: Tokenised carbon credits can be traded globally, without the need for centralised intermediaries. This makes the market more accessible and liquid, enabling participation from a broader range of investors, including individuals and smaller entities who previously faced barriers to entry. In South Africa, this could enhance carbon market liquidity by enabling broader, including international, participation in trading locally generated carbon credits.

Increased Accessibility and Liquidity: Tokenised carbon credits can be traded globally, without the need for centralised intermediaries. This makes the market more accessible and liquid, enabling participation from a broader range of investors, including individuals and smaller entities who previously faced barriers to entry. In South Africa, this could enhance carbon market liquidity by enabling broader, including international, participation in trading locally generated carbon credits.

Fractional Participation: By allowing the purchase of fractions of a carbon credit, tokenisation opens the market to retail investors and small businesses, enabling access to green finance solutions that were once limited to large institutions. In South Africa, this could allow SMEs subject to the Carbon Tax Act to purchase fractional carbon credits, lowering entry barriers to participation.

Automation and Efficiency: Smart contracts can automate processes like tracking, trading and retiring credits, which can lower transaction costs and complexity. Furthermore, by streamlining the process, tokenisation can help speed up the flow of capital to climate friendly projects. In South Africa, this could streamline the issuance, trading and retirement of credits, particularly for projects under programmes such as the Renewable Energy Independent Power Producer Procurement Programme, reducing administrative burdens.

Automation and Efficiency: Smart contracts can automate processes like tracking, trading and retiring credits, which can lower transaction costs and complexity. Furthermore, by streamlining the process, tokenisation can help speed up the flow of capital to climate friendly projects. In South Africa, this could streamline the issuance, trading and retirement of credits, particularly for projects under programmes such as the Renewable Energy Independent Power Producer Procurement Programme, reducing administrative burdens.

5. Regulatory Integration and Risks

The National Treasury has highlighted uncertainty over whether carbon credits (and tokenised forms) qualify as financial instruments under current law. A 2025 consultation proposes[19] formally recognising carbon credits within financial market regulation, potentially bringing tokenised credits under clearer rules on licensing, disclosure, market conduct and supervision, an important enabler for responsible green finance innovation.

If carbon credits are classified as financial instruments, market confidence and integration with mainstream finance may improve. However, several risks remain:

Greenwashing refers to the misrepresentation of financial products, services, or activities as environmentally sustainable when they do not meet genuine green criteria. In the context of tokenised carbon credits, greenwashing can occur if credits are marketed as supporting climate action but lack verifiable environmental impact or fail to meet regulatory standards.

Data manipulation involves the intentional distortion or falsification of climate or carbon credit data to mislead stakeholders. Within fintech enabled carbon markets, this risk includes altering project metrics, credit verification records or transaction histories to inflate environmental benefits or financial returns. Such manipulation can compromise the credibility of tokenised credits and the effectiveness of green finance.

Cybersecurity threats encompass risks of unauthorised access, data breaches, hacking and other malicious activities targeting digital platforms, blockchain registries and smart contracts used in carbon markets. Such risks may lead to the loss or theft of carbon credits, manipulation of transaction records or disruption of trading platforms, thereby undermining market integrity and confidence.

Interoperability challenge refers to difficulties in ensuring that different fintech platforms, blockchain networks and regulatory systems can communicate and operate seamlessly together. In the context of tokenised carbon credits, lack of interoperability may hinder the transfer, verification, and retirement of credits across markets and jurisdictions, limiting scalability and efficiency.

Mitigating these risks will require public–private coordination that aligns innovation with oversight. Independent audits, technology-enabled monitoring (including anomaly detection), and common standards can strengthen transparency. For South Africa, this also implies building domestic measurement, reporting, and verification as well as audit capacity alongside market-surveillance capabilities.

6. Conclusion: From Innovation to Integration

Fintech can strengthen green finance by improving transparency, trust and access rather than replacing existing structures. Tokenised carbon credits illustrate how digital infrastructure may lower transaction costs, improve data integrity, and broaden participation in markets that have historically struggled with credibility and scale.

In South Africa, the value of these innovations depends on their integration into sustainable finance frameworks, supported by robust verification standards, clear governance and effective supervision. Realising this potential will require alignment with existing carbon market mechanisms, particularly under the Carbon Tax Act, as well as regulatory clarity on the treatment of tokenised credits within financial market frameworks.

National Treasury initiatives, including the development of a national green finance taxonomy, provide an important foundation to align digital innovation with environmental objectives. In parallel, policy tools such as regulatory sandboxes and strengthened oversight of digital market infrastructure can support responsible innovation while safeguarding market integrity. If embedded well, tokenisation can act as enabling infrastructure that supports credible decarbonisation and adaptation while remaining consistent with financial stability and just transition goals.

[1] The authors are grateful to Sarah McPhail, Lead Economist at the South African Reserve Bank, for her thoughtful guidance and expertise throughout the development of this blog.

[2] Basel Committee on Banking Supervision: Climate related risk drivers and their transmission channels. Available

here

[3] NGFS Climate Scenarios for central banks and supervisors. Available

here

[4] Task Force on Climate-related Financial Disclosures (TCFD, 2017). Available

here.

[5] IFRS Foundation / ISSB (2023). Available

here.

[6] The World Bank defines green finance as the use of financial instruments and investments to support activities that improve environmental outcomes, particularly in areas such as renewable energy, energy efficiency, ecosystem conservation and climate resilience.

[7] The World Bank defines carbon credits as tradable instruments representing verified reductions or removals of greenhouse gas emissions, typically measured in tons of CO₂ equivalent and are issued following independent measurement, reporting and verification. Furthermore, carbon credits are used in both compliance and voluntary carbon markets to support emissions mitigation and mobilise green finance.

[8] World Bank (2022). Fintech and Financial Inclusion Reports. Available

here.

[9] World Bank / IFC–aligned literature (via Springer, 2025).

The nexus between fintech and green finance in advancing sustainable performance across countries

[10] Multilateral institutions consistently identify scale requirements, transaction costs, information asymmetries, and illiquid markets as key barriers limiting retail and SME participation in green and sustainable finance, with most instruments designed for institutional investors rather than smaller participants (OECD (2021) ,

Green Finance and Investment; World Bank (2020),

Green Finance: A Bottom‑Up Approach to Track Existing Flows).

[11] World Bank & IFC (2022).

Fintech and SME Finance: Expanding Responsible Access

[12] News24 , “Using carbon credits to boost Africa's economy and cut emissions" accessed on 2 December 2025.

[13] For example , see

Combatting Climate Change Through Carbon Credits .

[14] For example, see Carbonplace's “The infrastructure behind scalable carbon markets"

[15] Actively Managed Certificates (AMCs) are a type of structured financial product that tracks the performance of an underlying, actively managed portfolio of securities, such as stocks or bonds. They are issued by regulated institutions, are listed on exchanges, and offer a way for investors to gain exposure to a specific investment strategy without directly buying the individual assets.

[16] This type of insurance provides financial protection to the directors and officers of a company against claims made for alleged wrongful acts in their capacity as company leaders. In the context of carbon credits and climate-related risks, insurers may consider whether companies with carbon offsets are less exposed to certain risks when underwriting policies.

[17] Standard Bank Group. (2024).

Using carbon credits to boost Africa's economy and cut emissions.

Standard Bank Group Corporate & Investment Banking. (2025).

Combatting climate change through carbon credits. Sofala Partners. (2025).

Voluntary carbon markets in Sub‑Saharan Africa: What we are watching in 2025.

Orpheus Capital. (2024).

Carbon credit AMC brings global‑grade climate finance to South African mining and institutional investors.

Mining Business Africa. Howden Group. (2024).

Carbon credit warranty and indemnity insurance.

[18] World Bank. (2024).

Tokenization of Carbon Credits: Opportunities, Risks, and Market Integrity in Digital Environmental Assets. Climate Market Innovation Serie.

[19] See, National Treasury's Media Statement , “Treasury on developing the South African carbon credit market".

Disclaimer: As the IFWG we are enthusiastic to include diverse voices through our media content. The opinions of participants do not necessarily represent the views of the IFWG and their respective organisations.

Disclaimer: As the IFWG we are enthusiastic to include diverse voices through our media content. The opinions of participants do not necessarily represent the views of the IFWG and their respective organisations.